Wolfram Function Repository

Instant-use add-on functions for the Wolfram Language

Function Repository Resource:

Perform Bayesian linear regression with conjugate priors

ResourceFunction["BayesianLinearRegression"][{{var11,var12,…,y1},{var21,var22,…,y2},…},{f1,f2,…},{var1,var2,…}] performs a Bayesian linear model fit on the data using basis functions fi with independent variables vari. | |

ResourceFunction["BayesianLinearRegression"][{{var11,var12,…}→y1,{var21,var22,…}→y2,…},…] generates the same result. | |

ResourceFunction["BayesianLinearRegression"][{{var11,var12,…},{var21,var22,…},…}→{y1,y2,…},…] generates the same result. |

| "PriorParameters" | values of the hyperparameters corresponding to the prior distribution of the fit coefficients. |

| "PosteriorParameters" | values of the hyperparameters corresponding to the posterior distribution of the fit coefficients. |

| "LogEvidence" | the natural log of the marginal likelihood |

| "Prior" | prior distributions. |

| "Posterior" | posterior distributions. |

| "Basis" | the basis functions supplied by the user. |

| "IndependentVariables" | the independent variables supplied by the user. |

| "Functions" | functions that yield distributions when applied arbitrary hyperparameters; only included when the "IncludeFunctions"→True option is set. |

| "PredictiveDistribution" | predictive distribution of the data. |

| "UnderlyingValueDistribution" | the distribution of of the fit line of the data. |

| "RegressionCoefficientDistribution" | marginal distribution of the fit coefficients. |

| "ErrorDistribution" | marginal distribution of the variance (for 1D regression) or covariance matrix. |

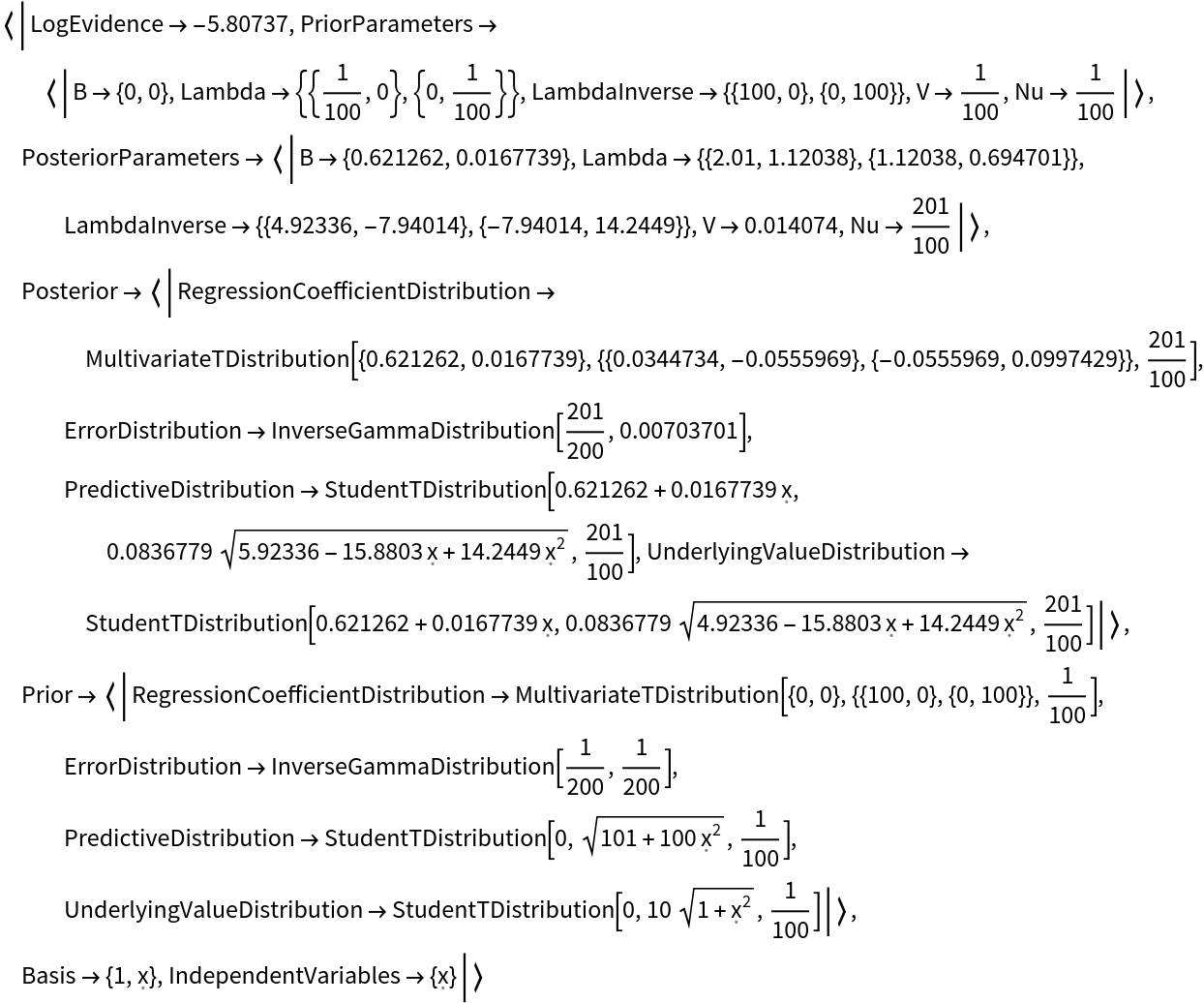

Generate a Bayesian linear regression on random data:

| In[1]:= |

| Out[1]= |  |

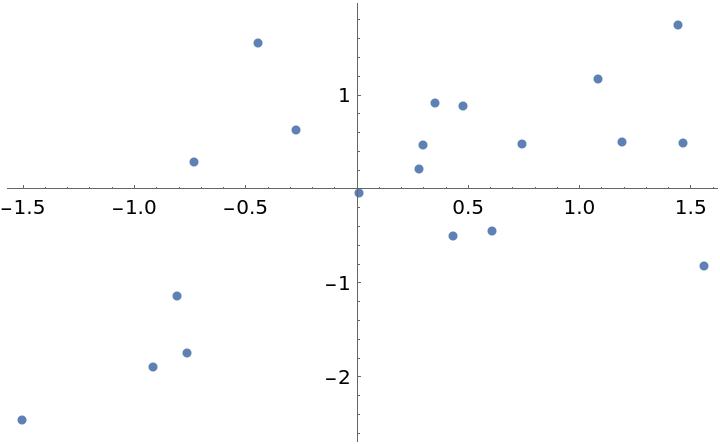

Generate test data:

| In[2]:= | ![data = RandomVariate[

MultinormalDistribution[( {

{1, 0.7},

{0.7, 1}

} )],

20

];

ListPlot[data]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/016164ebf0d34671.png) |

| Out[2]= |  |

Fit the data with a first-order polynomial:

| In[3]:= |

| Out[3]= |

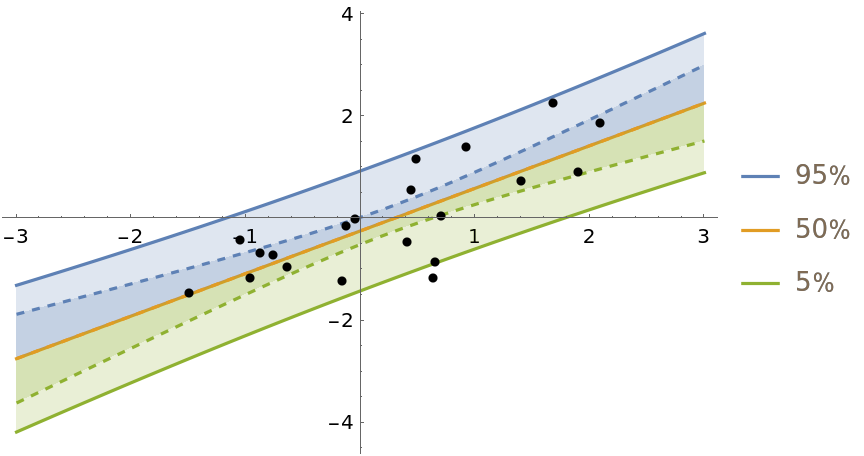

Show the predictive distribution of the model and the distribution of the fit line (dashed):

| In[4]:= | ![Show[

Plot[Evaluate@

InverseCDF[

linearModel["Posterior", "PredictiveDistribution"], {0.95, 0.5, 0.05}], {\[FormalX], -3, 3}, Filling -> {1 -> {2}, 3 -> {2}}, PlotLegends -> Table[Quantity[i, "Percent"], {i, {95, 50, 5}}]],

Plot[Evaluate@

InverseCDF[

linearModel["Posterior", "UnderlyingValueDistribution"], {0.95, 0.5, 0.05}], {\[FormalX], -3, 3}, Filling -> {1 -> {2}, 3 -> {2}}, PlotStyle -> Dashed],

ListPlot[data, PlotStyle -> Black],

PlotRange -> All

]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/5a73fe47f85494d0.png) |

| Out[4]= |  |

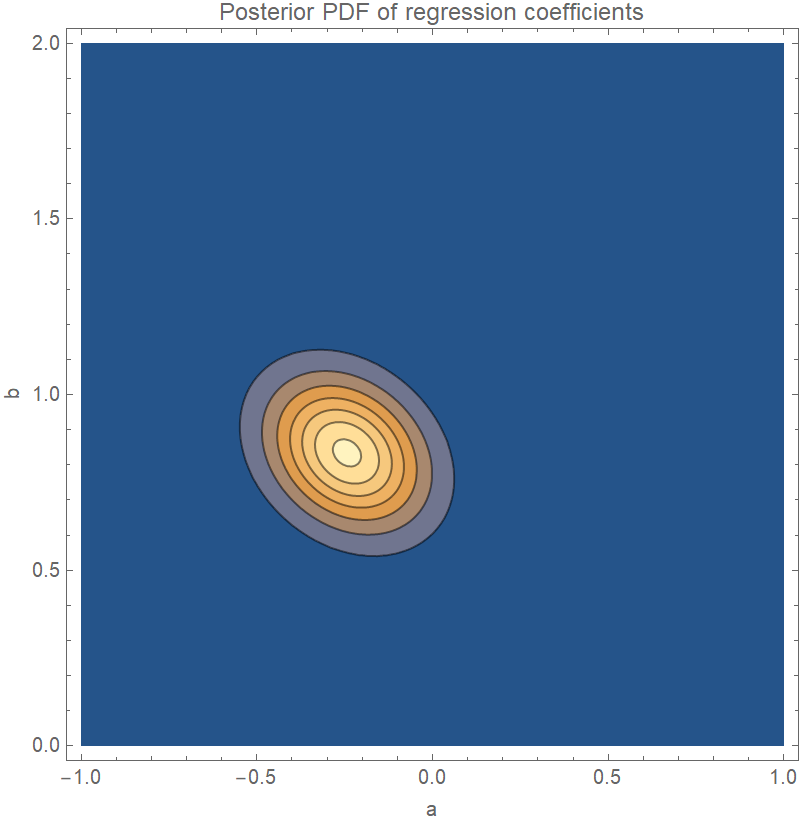

Plot the joint distribution of the coefficients a and b in the regression equation y=ax+b:

| In[5]:= | ![With[{

coefficientDist = linearModel["Posterior", "RegressionCoefficientDistribution"]

},

ContourPlot[

Evaluate[PDF[coefficientDist, {a, b}]],

{a, -1, 1},

{b, 0, 2},

PlotRange -> {0, All}, PlotPoints -> 20, FrameLabel -> {"a", "b"}, ImageSize -> 400,

PlotLabel -> "Posterior PDF of regression coefficients"

]

]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/325ce298ce1532ae.png) |

| Out[5]= |  |

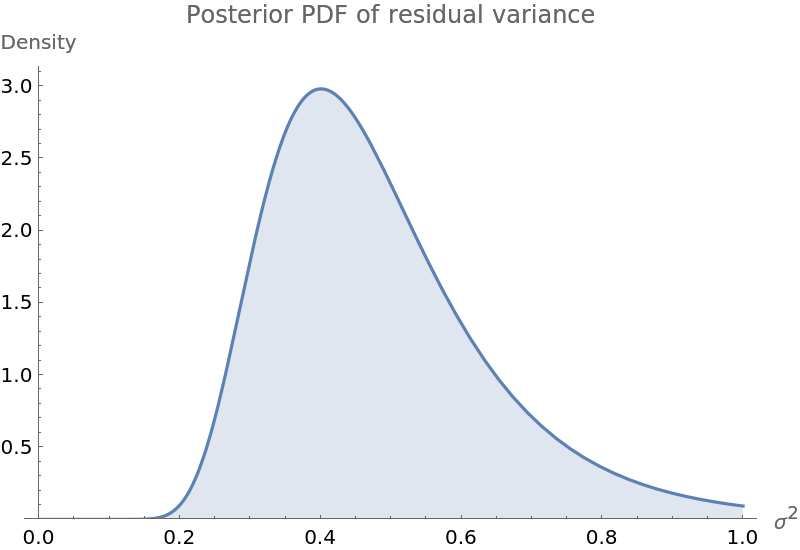

Plot the PDF of the posterior variance of the residuals:

| In[6]:= | ![With[{

errDist = linearModel["Posterior", "ErrorDistribution"]

},

Quiet@Plot[

Evaluate[PDF[errDist, e]],

{e, 0, 1},

PlotRange -> {0, All}, AxesLabel -> {"\!\(\*SuperscriptBox[\(\[Sigma]\), \(2\)]\)", "Density"}, ImageSize -> 400,

Filling -> Axis,

PlotLabel -> "Posterior PDF of residual variance"

]

]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/270e84b3f406a28b.png) |

| Out[6]= |  |

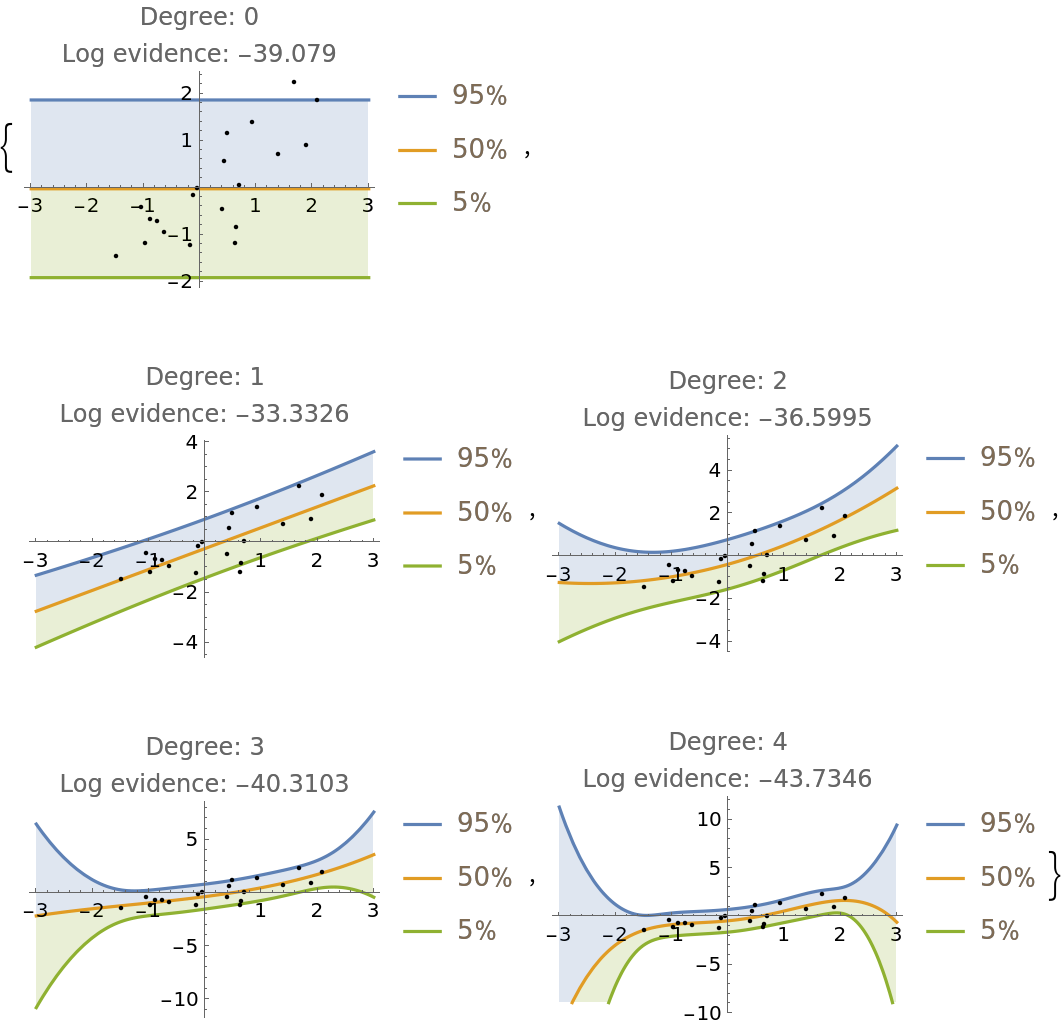

Fit the data with a polynomial of arbitrary degree and compare the prediction bands and log-evidence of fits up to degree 4:

| In[7]:= | ![Table[

Module[{

model = ResourceFunction["BayesianLinearRegression"][

Rule @@@ data, \[FormalX]^Range[0, degree], \[FormalX]],

predictiveDist

},

predictiveDist = model["Posterior", "PredictiveDistribution"];

Show[

Plot[Evaluate@

InverseCDF[predictiveDist, {0.95, 0.5, 0.05}], {\[FormalX], -3, 3}, Filling -> {1 -> {2}, 3 -> {2}}, PlotLegends -> Table[Quantity[i, "Percent"], {i, {95, 50, 5}}]],

ListPlot[data, PlotStyle -> Black],

PlotRange -> All,

PlotLabel -> StringForm["Degree: `1`\nLog evidence: `2`", degree, model["LogEvidence"] ]

]

],

{degree, 0, 4}

]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/761192f7aeeeb8ad.png) |

| Out[7]= |  |

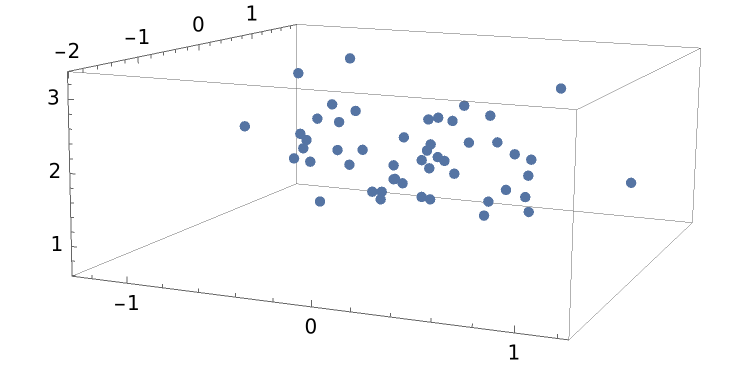

BayesianLinearRegression can do multivariate regression. For example, generate some 3D data:

| In[8]:= | ![data = RandomVariate[

MultinormalDistribution[{0, 0, 2}, RandomVariate[

InverseWishartMatrixDistribution[5, IdentityMatrix[3]]]],

50

];

ListPointPlot3D[data]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/207039f1a9b8f473.png) |

| Out[8]= |  |

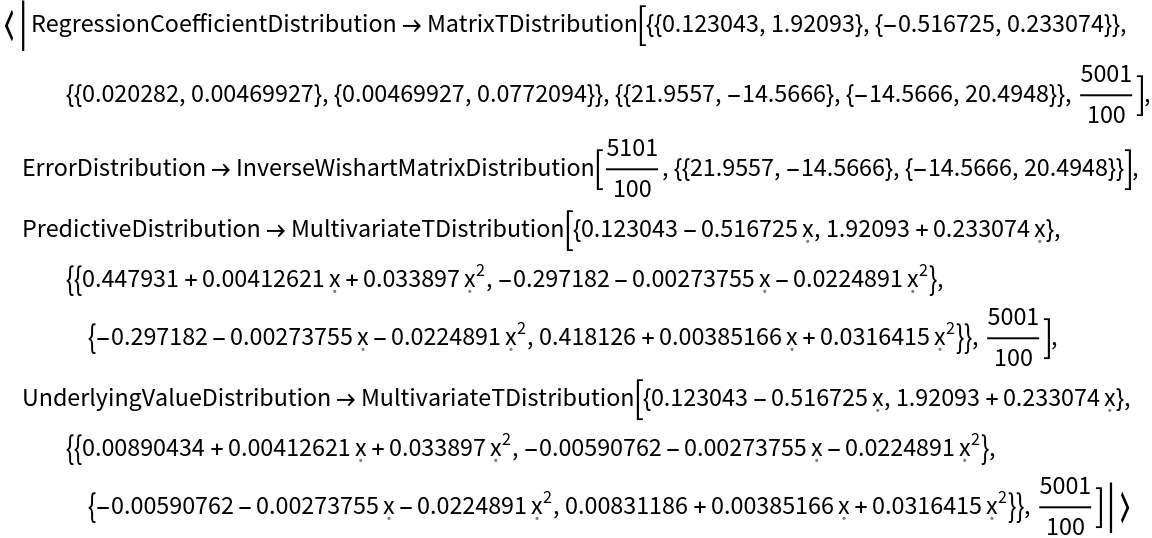

Do a regression where the x-coordinate is treated as the independent variable and y and z are both dependent on x:

| In[9]:= |

| Out[9]= |  |

The predictive joint distribution for y and z is a MultivariateTDistribution:

| In[10]:= |

| Out[10]= |  |

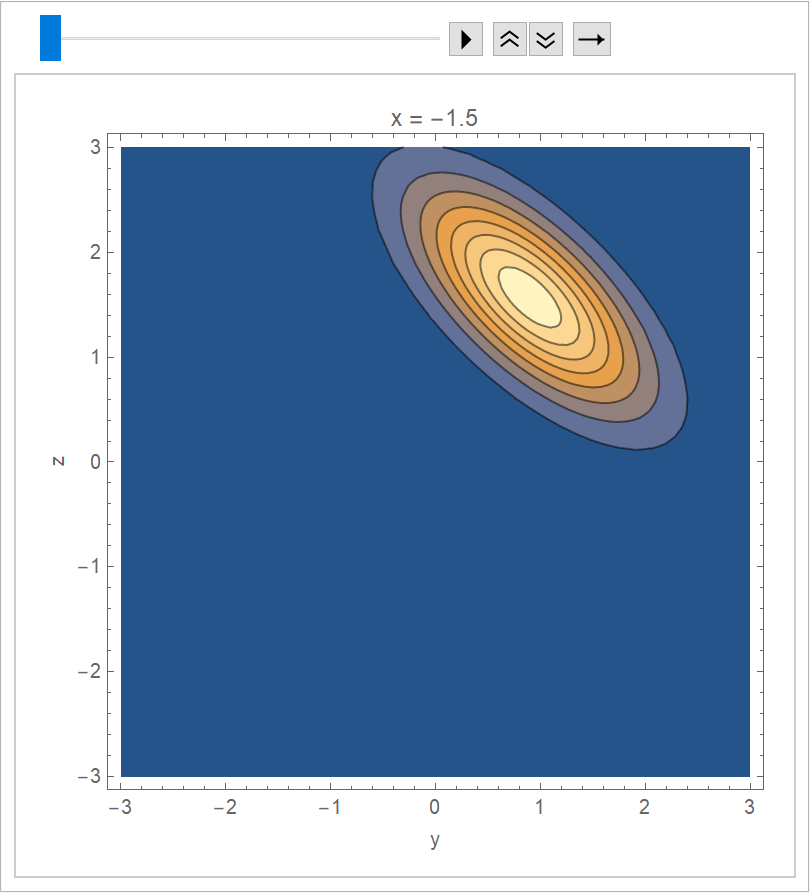

Visualize the joint distribution as an animation:

| In[11]:= | ![ListAnimate[

Table[

ContourPlot[

Evaluate[PDF[multiRegressionDist, {y, z}]],

{y, -3, 3},

{z, -3, 3},

PlotRange -> All,

FrameLabel -> {"y", "z"},

PlotLabel -> StringForm["x = `1`", \[FormalX]],

PlotPoints -> 20

],

{\[FormalX], -1.5, 1.5, 0.1}

],

AnimationRunning -> False

]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/01a08f6768f87389.png) |

| Out[11]= |  |

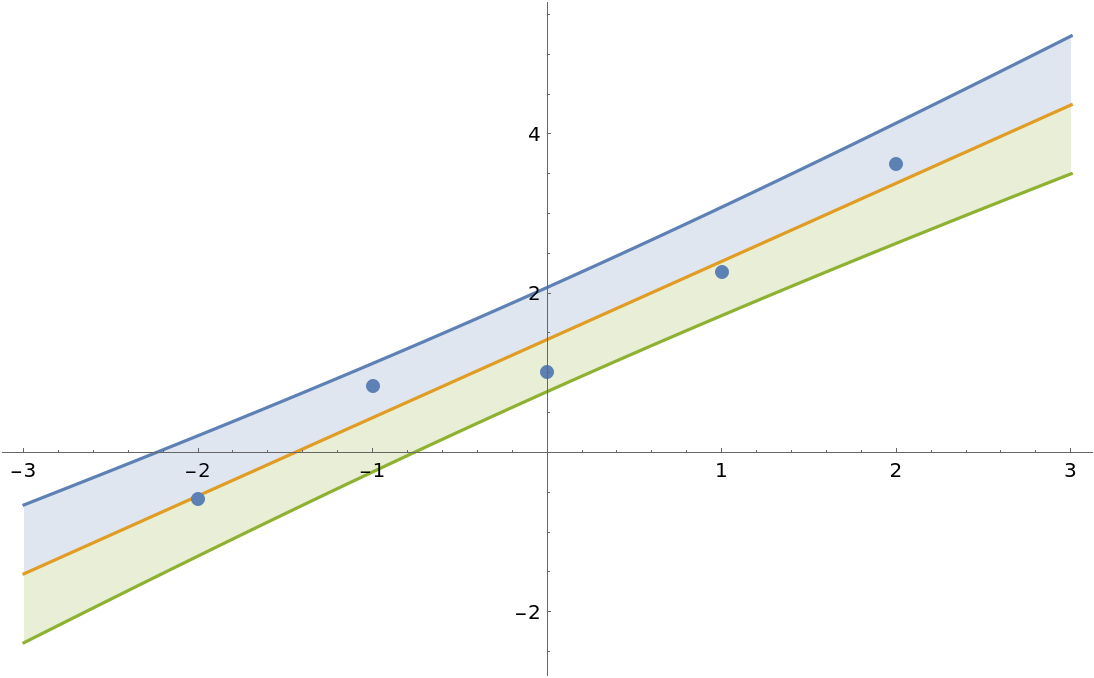

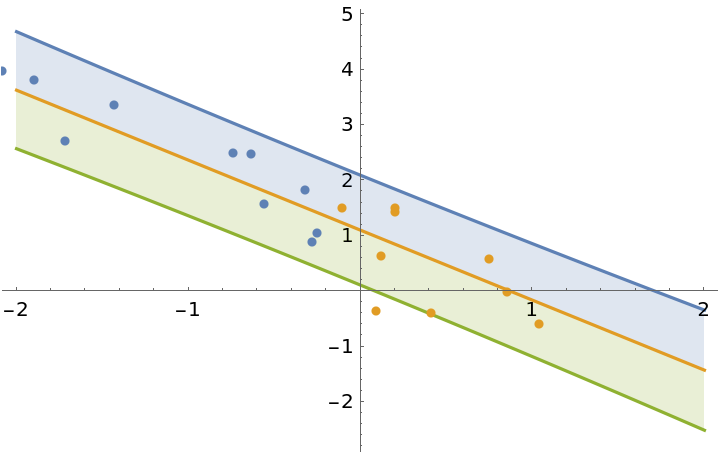

Just like LinearModelFit, BayesianLinearRegression constructs a model with bias term by default:

| In[12]:= | ![data = Range[-2, 2] -> Range[-2, 2] + 1 + RandomVariate[NormalDistribution[], 5];

model = ResourceFunction["BayesianLinearRegression"][

data, \[FormalX], \[FormalX]];

Show[

Plot[

Evaluate[

InverseCDF[

model["Posterior", "PredictiveDistribution"], {0.95, 0.5, 0.05}]],

{\[FormalX], -3, 3},

Filling -> {1 -> {2}, 3 -> {2}}

],

ListPlot[Transpose[List @@ data]]

]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/4b7ff1cb0f646f39.png) |

| Out[12]= |  |

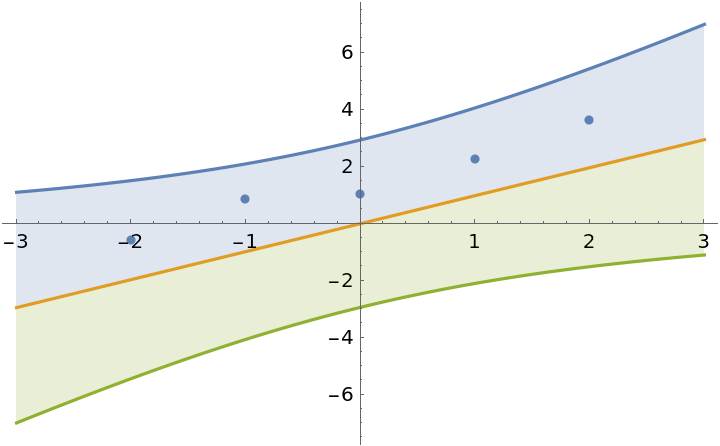

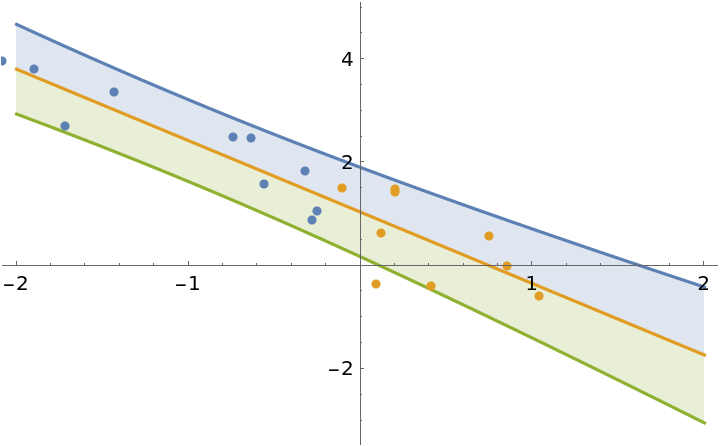

Force the intercept to be zero:

| In[13]:= | ![model2 = ResourceFunction["BayesianLinearRegression"][

data, \[FormalX], \[FormalX], IncludeConstantBasis -> False];

Show[

Plot[

Evaluate[

InverseCDF[

model2["Posterior", "PredictiveDistribution"], {0.95, 0.5, 0.05}]],

{\[FormalX], -3, 3},

Filling -> {1 -> {2}, 3 -> {2}}

],

ListPlot[Transpose[List @@ data]]

]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/7218cb068b47830a.png) |

| Out[13]= |  |

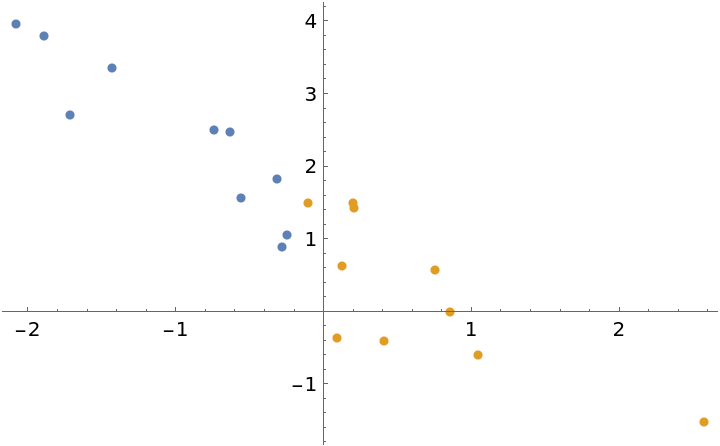

The prior can be specified in the same format as the parameter outputs of the Bayesian linear regression. This can be used to update a model with new observations. To illustrate this, generate some test data and divide the dataset into two parts:

| In[14]:= | ![data = TakeDrop[ SortBy[First]@RandomVariate[MultinormalDistribution[{0, 1}, ( {

{1, -1.3},

{-1.3, 2}

} )], 20], 10];

plot = ListPlot[data]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/2c1645f7fe636efd.png) |

| Out[14]= |  |

Fit the first half of the data:

| In[15]:= | ![model1 = ResourceFunction["BayesianLinearRegression"][

Rule @@@ data[[1]], \[FormalX], \[FormalX]];

Show[

Plot[Evaluate@InverseCDF[

model1["Posterior", "PredictiveDistribution"],

{0.95, 0.5, 0.05}

], {\[FormalX], -2, 2}, Filling -> {1 -> {2}, 3 -> {2}}],

plot

]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/389f4e144c3e1b9d.png) |

| Out[15]= |  |

Use the posterior parameters of model1 as the prior to update the model with the second half of the dataset:

| In[16]:= | ![model2 = ResourceFunction["BayesianLinearRegression"][

Rule @@@ data[[2]], \[FormalX], \[FormalX], "PriorParameters" -> model1["PosteriorParameters"]];

Show[

Plot[Evaluate@InverseCDF[

model2["Posterior", "PredictiveDistribution"],

{0.95, 0.5, 0.05}

], {\[FormalX], -2, 2}, Filling -> {1 -> {2}, 3 -> {2}}],

plot

]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/0aa2b3d6145b2964.png) |

| Out[16]= |  |

The result is exactly the same as when you would fit all of the data in a single step:

| In[17]:= | ![model3 = ResourceFunction["BayesianLinearRegression"][

Rule @@@ (Join @@ data), \[FormalX], \[FormalX]];

Column[{

model3["PosteriorParameters"],

model2["PosteriorParameters"]

}]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/38ff06b0dae9eb35.png) |

| Out[17]= |  |

When "IncludeFunctions"→True, the returned association contains the key "Functions". This key holds the functions that can be used to generate distributions from arbitrary values of hyperparameters:

| In[18]:= | ![data = Range[-2, 2] -> Range[-2, 2] + RandomVariate[NormalDistribution[], 5];

model = ResourceFunction["BayesianLinearRegression"][

data, \[FormalX], \[FormalX], "IncludeFunctions" -> True];

Keys@model["Functions"]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/369285418a9ea4cc.png) |

| Out[18]= |

The posterior distribution is obtained from the predictive distribution function:

| In[19]:= |

| Out[19]= |

Apply it to the posterior parameters:

| In[20]:= |

| Out[20]= |

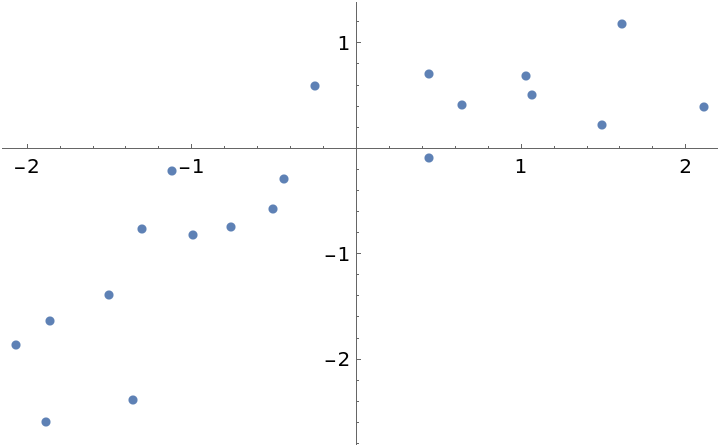

Here is a dataset where it is unclear if the fit should be first or second order:

| In[21]:= |

| Out[21]= |  |

Fit the data with polynomials up to fourth degree, rank the log-evidences and inspect them:

| In[22]:= | ![models = AssociationMap[

ResourceFunction["BayesianLinearRegression"][

Rule @@@ data, \[FormalX]^Range[0, #], \[FormalX]] &,

Range[0, 4]

];

ReverseSort@models[[All, "LogEvidence"]]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/45ba2609062bcb9c.png) |

| Out[22]= |

Calculate the weights for each fit:

| In[23]:= | ![weights = Normalize[

(* subtract the max to reduce rounding error *)

Exp[models[[All, "LogEvidence"]] - Max[models[[All, "LogEvidence"]]]],

Total

];

ReverseSort[weights]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/2b22dbe61b9bbbbd.png) |

| Out[23]= |

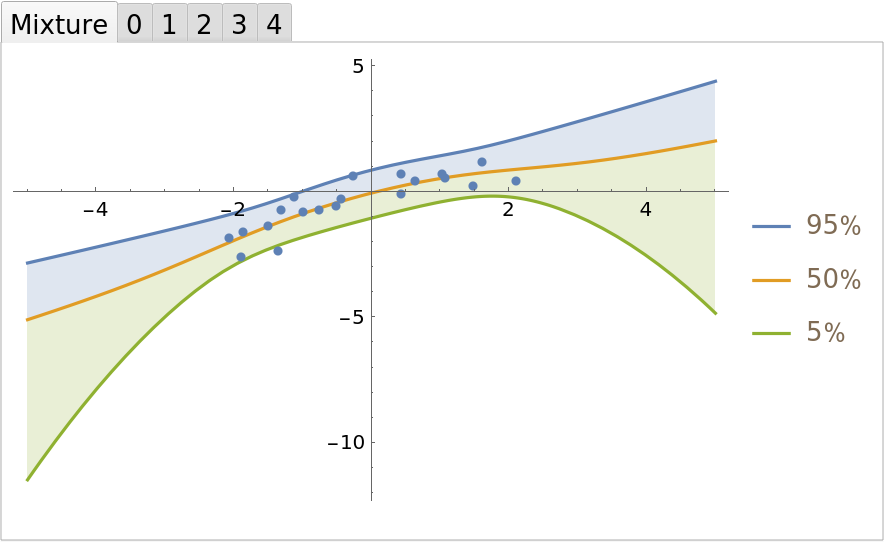

Because the weights for the first and second order fits are so close, the correct Bayesian treatment is to include both in the final regression. Define a mixture of posterior predictive distributions:

| In[24]:= | ![mixDist = MixtureDistribution[

Values[weights],

Values@models[[All, "Posterior", "PredictiveDistribution"]]

];

Short /@ mixDist](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/478035e1f8d15b19.png) |

| Out[24]= |  |

Compare the mixture fit to the individual polynomial regressions:

| In[25]:= | ![TabView[

KeyValueMap[

#1 -> Show[

Plot[

Evaluate@InverseCDF[#2, {0.95, 0.5, 0.05}],

{\[FormalX], -5, 5},

Filling -> {1 -> {2}, 3 -> {2}}, PlotLegends -> Table[Quantity[i, "Percent"], {i, {95, 50, 5}}],

PlotLabel -> Replace[

Lookup[weights, #1, None],

n_?NumericQ :> StringForm["Weight: `1`", n]

]

],

plot

] &,

Prepend[

models[[All, "Posterior", "PredictiveDistribution"]],

"Mixture" -> mixDist

]

]

]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/5c40921314363285.png) |

| Out[25]= |  |

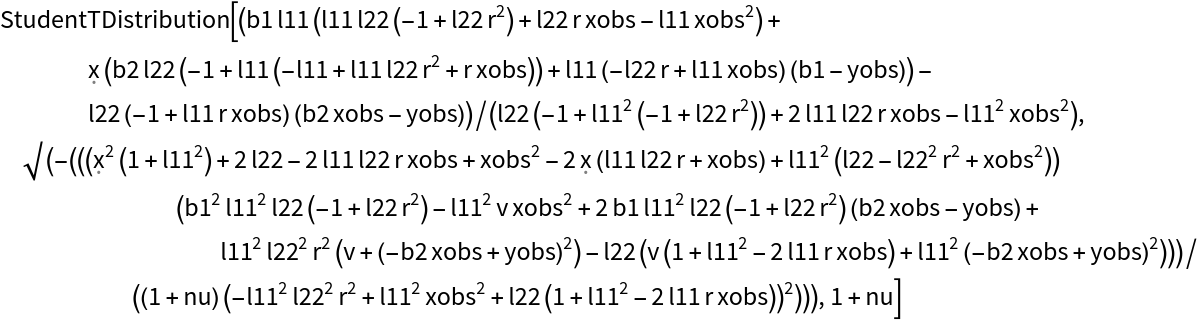

Symbolically calculate the predictive posterior after a single observation for any prior:

| In[26]:= | ![model = ResourceFunction[

"BayesianLinearRegression"][{xobs -> yobs}, \[FormalX], \[FormalX],

"PriorParameters" -> <|"B" -> {b1, b2}, "Lambda" -> {{l11^2, r l11 l22}, {r l11 l22, l22}}, "V" -> v, "Nu" -> nu|>];

dist[{xobs_, yobs_}, {b1_, b2_}, {l11_, l22_, r_}, v_, nu_] = Assuming[

v > 0 && nu > 0 && {xobs, yobs, \[FormalX], b1, b2, l11, l22} \[Element] Reals && -1 < r < 1,

FullSimplify[model["Posterior", "PredictiveDistribution"]]

]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/66c9d40827009890.png) |

| Out[26]= |  |

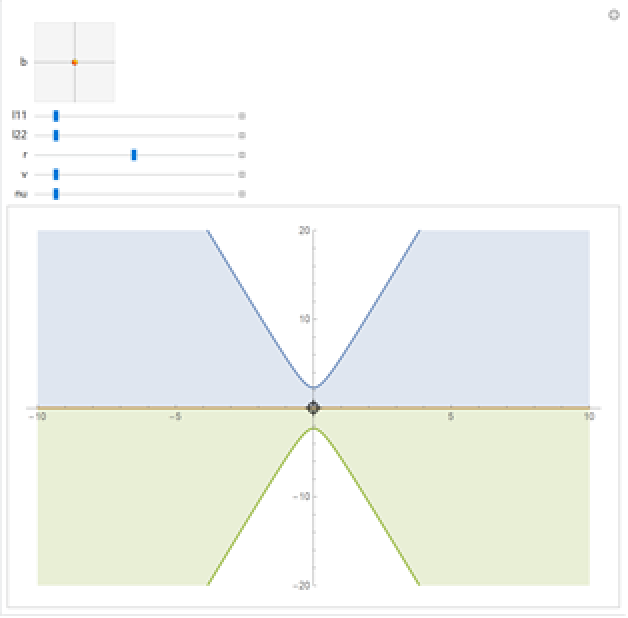

Visualize the prediction bands:

| In[27]:= | ![Manipulate[

Plot[

Evaluate@Thread@Tooltip[

InverseCDF[

dist[pt, b, {Sqrt[l11], Sqrt[l22], r}, v, nu], {0.95, 0.5, 0.05}],

Table[Quantity[i, "Percent"], {i, {95, 50, 5}}]

],

{\[FormalX], -10, 10},

PlotRange -> {-20, 20},

ImageSize -> Large,

Filling -> {1 -> {2}, 3 -> {2}}

],

{{pt, {0, 0}}, {-10, -10}, {10, 10}, ControlType -> Locator},

{{b, {0, 0}}, {-10, -10}, {10, 10}},

{{l11, 0.01}, 0.0001, 0.1},

{{l22, 0.01}, 0.0001, 0.1},

{{r, 0}, -1, 1},

{{v, 0.1}, 0.0001, 1},

{{nu, 0.1}, 0.0001, 1},

SaveDefinitions -> True

]](https://www.wolframcloud.com/obj/resourcesystem/images/c66/c66f7392-efcc-42ca-949e-311fe403fb99/66d8e6ad5778d3e3.png) |

| Out[27]= |  |

This work is licensed under a Creative Commons Attribution 4.0 International License