Wolfram Function Repository

Instant-use add-on functions for the Wolfram Language

Function Repository Resource:

Calculate conditional and marginal distributions of the multivariate normal distribution

ResourceFunction["ConditionedMultinormalDistribution"][MultinormalDistribution[μ,Σ],i→xi] returns the MultinormalDistribution obtained by conditioning coordinate i to value xi. | |

ResourceFunction["ConditionedMultinormalDistribution"][…,{i1→xi1,i2→xi2,…}] conditions on multiple coordinates. | |

ResourceFunction["ConditionedMultinormalDistribution"][…,{i1,i2,…}→{xi1,xi2,…}] can also be used. | |

ResourceFunction["ConditionedMultinormalDistribution"][…,…,{n1,n2,…}] returns the marginal distributions of coordinates ni after conditioning. | |

ResourceFunction["ConditionedMultinormalDistribution"][Inactive[MultinormalDistribution][…],…] works with SparseArray and SymmetrizedArray objects. |

Condition a 2D symbolic multivariate normal distribution on the value of the second coordinate:

| In[1]:= |

| Out[2]= |

A NormalDistribution is returned if you specify that the first marginal should be computed:

| In[3]:= |

| Out[3]= |

Generate a random MultinormalDistribution:

| In[4]:= | ![randomDist = With[{dim = 10},

MultinormalDistribution[

RandomReal[{-10, 10}, dim],

RandomVariate[

InverseWishartMatrixDistribution[dim + 1, IdentityMatrix[dim]]]

]

];](https://www.wolframcloud.com/obj/resourcesystem/images/325/3250a8e9-b3ee-4318-9ed0-02fc665ed0fc/11027453546640a3.png) |

Calculate how the expected value of the second coordinate depends on the value of the first:

| In[5]:= |

| Out[5]= |

Calculate the derivative:

| In[6]:= |

| Out[6]= |

Condition on multiple indices and obtain the means of multiple marginals:

| In[7]:= |

| Out[7]= |

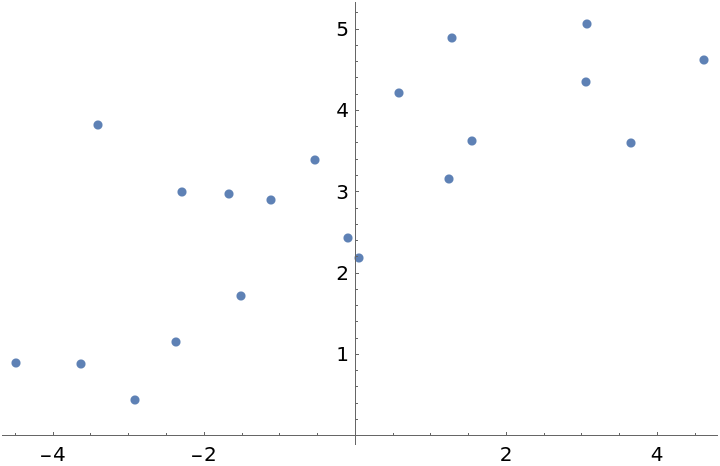

Generate some (x,y) data:

| In[8]:= |

| Out[9]= |  |

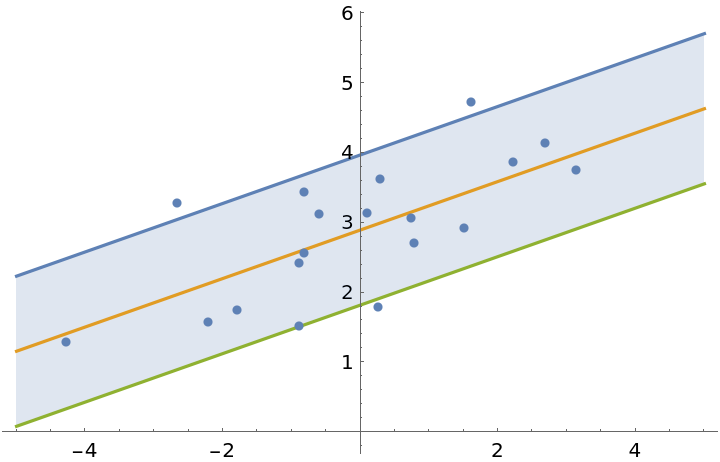

Perform a simple linear fit by estimating the joint distribution of the data and then condition it on x:

| In[10]:= | ![dist = Simplify@ResourceFunction["ConditionedMultinormalDistribution"][

EstimatedDistribution[data, MultinormalDistribution[{\[Mu]1, \[Mu]2}, {{\[CapitalSigma]11, \[CapitalSigma]12}, {\[CapitalSigma]12, \[CapitalSigma]22}}]],

1 -> \[FormalX],

2]](https://www.wolframcloud.com/obj/resourcesystem/images/325/3250a8e9-b3ee-4318-9ed0-02fc665ed0fc/7ff81c296459c9a6.png) |

| Out[10]= |

Plot the result:

| In[11]:= | ![Show[

Plot[Evaluate@InverseCDF[dist, {0.95, 0.5, 0.05}], {\[FormalX], -5, 5}, Filling -> {1 -> {3}}],

ListPlot[data]]](https://www.wolframcloud.com/obj/resourcesystem/images/325/3250a8e9-b3ee-4318-9ed0-02fc665ed0fc/7db63f04693bd05d.png) |

| Out[11]= |  |

MultinormalDistribution normally converts SparseArray and StructuredArray objects to regular lists:

| In[12]:= |

| Out[13]= |  |

Use Inactive to keep the covariance matrix packed as a sparse array:

| In[14]:= | ![ResourceFunction["ConditionedMultinormalDistribution"][

Inactive[MultinormalDistribution][sparseCovariance],

1 -> 2

] // RepeatedTiming](https://www.wolframcloud.com/obj/resourcesystem/images/325/3250a8e9-b3ee-4318-9ed0-02fc665ed0fc/42d4ae29a8fd0431.png) |

| Out[14]= |

This is significantly more computationally efficient than having the covariance unpack into a regular list:

| In[15]:= | ![ResourceFunction["ConditionedMultinormalDistribution"][

MultinormalDistribution[sparseCovariance],

1 -> 2

] // RepeatedTiming](https://www.wolframcloud.com/obj/resourcesystem/images/325/3250a8e9-b3ee-4318-9ed0-02fc665ed0fc/197d7a8137382e8a.png) |

| Out[15]= |  |

Conditioning on variables can be done with Conditioned, but it is less convenient and results in a general ProbabilityDistribution:

| In[16]:= | ![dist1 = ProbabilityDistribution[

{

"CDF",

Simplify@Probability[

x1 < \[FormalY] \[Conditioned] x2 == a,

{x1, x2} \[Distributed] MultinormalDistribution[{\[Mu]1, \[Mu]2}, {{\[CapitalSigma]11, \[CapitalSigma]12}, {\[CapitalSigma]12, \[CapitalSigma]22}}]

]

},

{\[FormalY], -\[Infinity], \[Infinity]}

]](https://www.wolframcloud.com/obj/resourcesystem/images/325/3250a8e9-b3ee-4318-9ed0-02fc665ed0fc/3f159176f7cffc6d.png) |

| Out[16]= |  |

The same distribution with ConditionedMultinormalDistribution:

| In[17]:= | ![dist2 = Simplify@

ResourceFunction["ConditionedMultinormalDistribution"][

MultinormalDistribution[{\[Mu]1, \[Mu]2}, {{\[CapitalSigma]11, \[CapitalSigma]12}, {\[CapitalSigma]12, \[CapitalSigma]22}}], 2 -> a, 1]](https://www.wolframcloud.com/obj/resourcesystem/images/325/3250a8e9-b3ee-4318-9ed0-02fc665ed0fc/71f3cb4c8d461ba4.png) |

| Out[17]= |

The PDFs are the same up to a minus sign under the square:

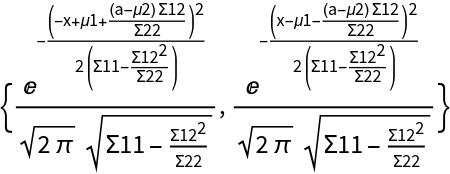

| In[18]:= | ![{

PDF[dist1, x],

PDF[dist2, x]

}](https://www.wolframcloud.com/obj/resourcesystem/images/325/3250a8e9-b3ee-4318-9ed0-02fc665ed0fc/209198539daa3a4f.png) |

| Out[18]= |  |

This work is licensed under a Creative Commons Attribution 4.0 International License