Wolfram Function Repository

Instant-use add-on functions for the Wolfram Language

Function Repository Resource:

Remove redundant data from a time series

ResourceFunction["TimeSeriesCompress"][tseries] compresses time series tseries by removing data points that can be accurately predicted through linear interpolation. |

| "ValueTolerance" | 10-10 | maximal allowed value deviation with respect to the original value |

| "MaxTimeDistance" | Infinity | maximal allowed time distance between two data points |

Create an example time series:

| In[1]:= |

| Out[1]= |

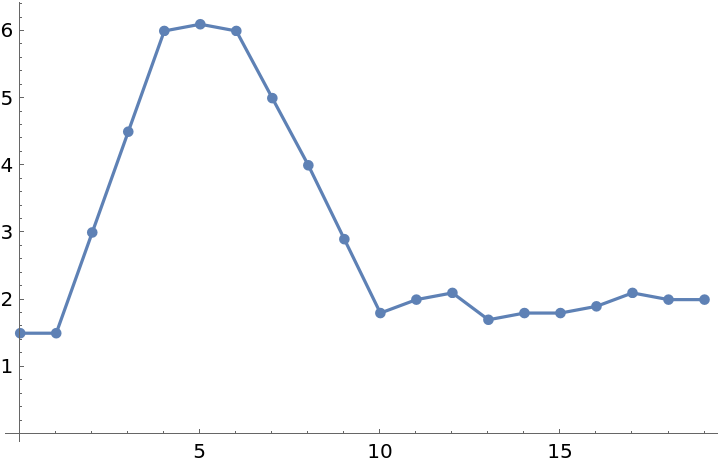

Visualize the path:

| In[2]:= |

| Out[2]= |  |

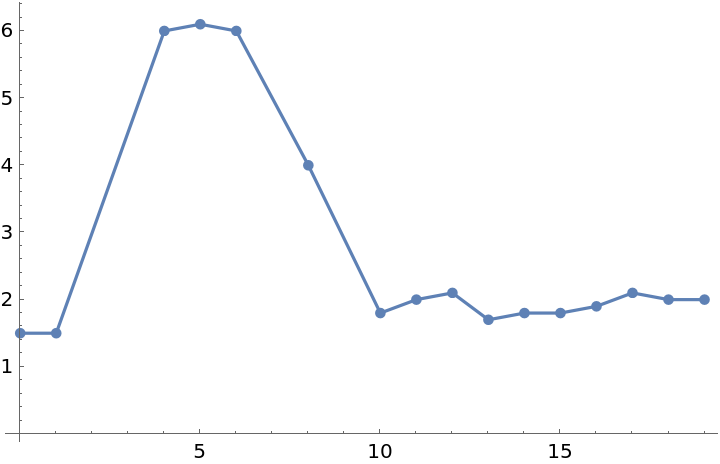

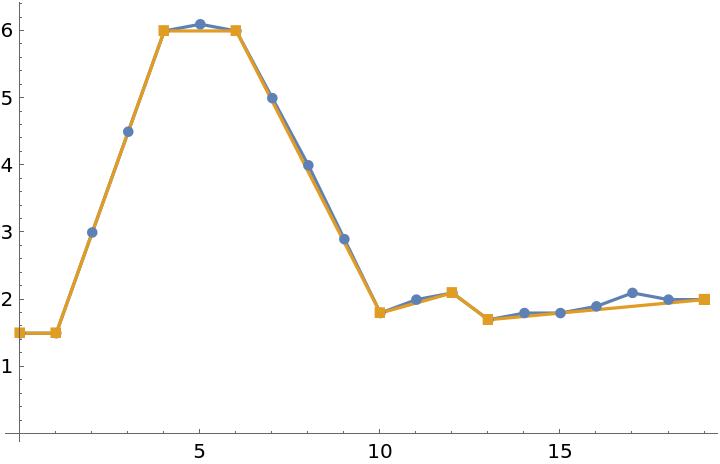

Four redundant points are removed from the time series by compression:

| In[3]:= |

| Out[3]= |  |

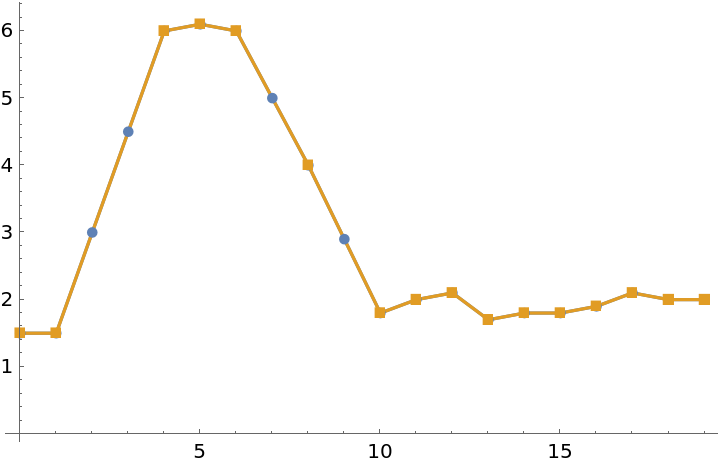

Visualize the removed points:

| In[4]:= |

| Out[4]= |  |

Compress a list of numeric values:

| In[5]:= |

| Out[5]= |

| In[6]:= |

| Out[6]= |

Compress a list of time-value pairs:

| In[7]:= |

| In[8]:= |

| Out[8]= |

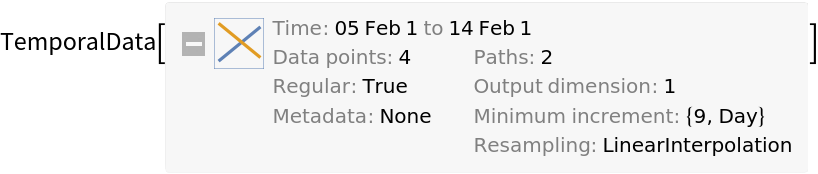

Compressing TemporalData applies compression to all underlying paths. The resampling is changed to linear interpolation:

| In[9]:= |

| Out[9]= |  |

Increasing the maximal allowed deviation in the time series value leads to better compression:

| In[10]:= |

| Out[10]= |

| In[11]:= |

| Out[11]= |

Visualize the removed points:

| In[12]:= |

| Out[12]= |  |

Backtesting the compressed time series values with the original time series values:

| In[13]:= |

| Out[13]= |

Limit the maximal time distance between two points:

| In[14]:= |

| Out[14]= |

TimeSeriesCompress only works on time series whose values are scalars. Time series with higher-dimensional values are returned uncompressed:

| In[15]:= |

| Out[15]= |

EventSeries is a special case of TemporalData allowing no interpolation. To compress an EventSeries, convert it to a TimeSeries:

| In[16]:= |

| Out[16]= |

TimeSeriesCompress removes values with head Missing:

| In[17]:= |

| Out[17]= |

| In[18]:= |

| Out[18]= |

Use TemporalData to store the stock prices of the FAANG companies since the beginning of the decade:

| In[19]:= |

| Out[19]= |

If you are not interested in cent fluctuations of the prices of these stocks, you can work with a compressed representation:

| In[20]:= |

| Out[20]= |

Compression reduces the required data points by about 40 percent:

| In[21]:= |

| Out[21]= |

This work is licensed under a Creative Commons Attribution 4.0 International License