In the Markowitz portfolio model, the goal is to balance expected return against risk. Each asset has its own average performance and volatility, but the overall portfolio behavior also depends on how the assets move together. When assets are imperfectly correlated, losses in some can be offset by gains in others, which allows diversification to reduce total risk.

Simulate daily percentage returns for six assets from a normal distribution and smooth each series with a moving average to reduce noise and obtain clearer return patterns:

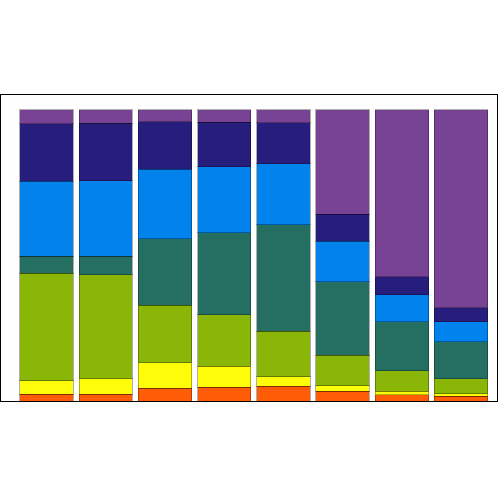

Compute the optimal risk–return pairs across a range of risk-aversion parameter values. Each solution gives an optimal portfolio, from which we extract its risk and expected return:

A diversified portfolio can be obtained for low risk aversion, but when the risk aversion is high, the market impact cost dominates, due to purchasing less diversified stock: